Forecasting

Every meaningful business decision is, at its core, a decision about the future.

When organizations hire new employees, expand production capacity, sign leases, launch products, acquire inventory, enter new markets, or make capital investments, they are making assumptions about what they believe will happen next. Forecasting is the process of evaluating those assumptions and translating them into an actionable view of the future.

As a discipline, forecasting serves many purposes. It helps organizations allocate resources, coordinate activities across departments, establish priorities, evaluate investment decisions, and align leadership around a common set of expectations. It provides the foundation upon which budgets, operating plans, staffing decisions, purchasing activities, and strategic initiatives are built.

Developing a meaningful forecast is rarely the responsibility of a single individual or department. Sales contributes customer and market expectations. Operations evaluates capacity and execution requirements. Human Resources assesses workforce needs. Procurement evaluates supplier capabilities and material availability. Finance consolidates assumptions into a financial view of future performance. Leadership contributes strategic priorities and organizational objectives.

The resulting forecast often reflects the collective judgment of people across the organization. In many companies, significant time and effort are invested in gathering information, challenging assumptions, reconciling competing priorities, and developing consensus around the most likely future outcome.

Because forecasts play such a central role in decision-making, it is worth considering what information an ideal forecast should provide.

Most organizations begin with the core outcomes that management needs to plan and operate the business:

- Revenue

- Margin

- EBITDA

- Cash flow

- Capital requirements

- Headcount requirements

- Departmental budgets

These measures remain essential because they translate business expectations into operational and financial plans.

An ideal forecast, however, extends beyond expected outcomes. It also helps decision makers understand the assumptions supporting those outcomes and the factors most likely to influence them.

In addition to projected results, an ideal forecast should provide visibility into:

- The assumptions that drive future performance

- The degree of confidence associated with those assumptions

- The risks that could materially affect outcomes

- The indicators that suggest conditions are changing

- The actions available to improve the likelihood of success

Taken together, these elements provide a more complete picture of the future. They help leadership understand not only what is expected to happen, but also why it is expected to happen, how confident the organization should be, and what factors deserve the greatest attention.

This perspective is increasingly reflected in modern forecasting practices. Researchers, finance professionals, and consulting firms have all emphasized the importance of scenario analysis, uncertainty management, and risk assessment as complements to traditional forecasting methods. The objective is not simply to estimate future outcomes, but to improve the quality of decisions made using those estimates.

Viewed through this lens, forecasting becomes more than a planning exercise. It becomes a mechanism for understanding the future, evaluating uncertainty, and making better decisions in the present.

Forecasting Confidence Depends on Certainty and Significance

Every forecast is built on assumptions; some assumptions are highly certain while others are not.

Just as importantly, some assumptions have a significant influence on future results, while others have very little impact on the forecast as a whole.

These two characteristics - certainty and significance - provide a useful framework for understanding forecast confidence.

Certainty reflects how confident the organization is that an assumption will prove correct.

Significance reflects how much the forecast would change if the assumption proves incorrect.

Statistical Confidence vs. Forecast Confidence

Before discussing forecast certainty, it is important to distinguish between two very different concepts that are often described using the same language.

Statistical confidence is derived from historical data and mathematical models. It asserts how likely a forecasted value is to fall within the predicted confidence interval.

Statistical confidence has an important limitation in that it primarily evaluates what has happened in the past. Businesses with commodities or consumer sales with a lot of data can benefit from this type of forecasting.

This article focuses on forecast confidence rather than statistical confidence.

Forecast confidence reflects the organization's belief that the assumptions supporting the forecast are likely to hold true. It incorporates information that may never appear in historical datasets, including customer sentiment, supplier performance, workforce stability, operational constraints, market changes, contractual obligations, and countless other factors that influence future outcomes.

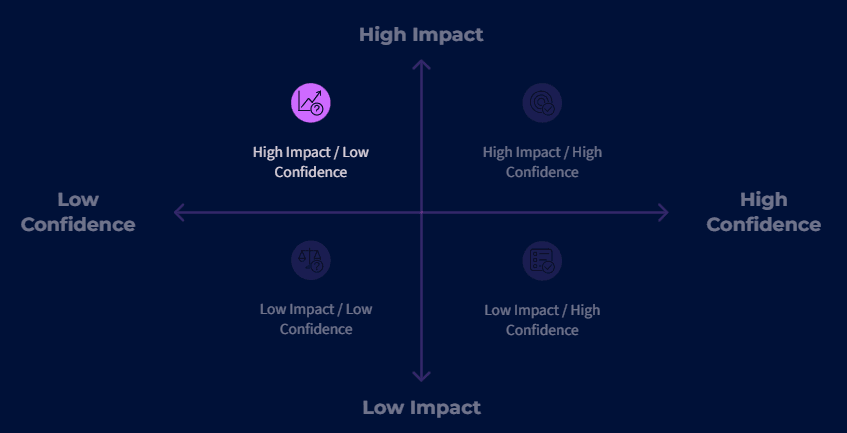

The Importance of Impact

Not all assumptions deserve the same level of attention.

An assumption about office supply expenses may carry relatively low certainty, but it is unlikely to have a material impact on profitability or cash flow. Conversely, an assumption regarding the renewal of a major customer may be highly certain, but because of its significance, even a small change in confidence deserves attention.

The assumptions that matter most are those that combine high significance with lower levels of certainty. These are the assumptions most capable of changing future outcomes.

Consider two companies that both forecast $50 million in annual revenue.

On the surface, the forecasts appear identical.

Yet the assumptions supporting them are dramatically different.

The first company has long-term customer contracts, diversified revenue streams, stable operations, and a predictable workforce. Most of the assumptions driving future performance are both significant and highly certain.

The second company relies on several large opportunities that have not yet closed, a handful of customers showing signs of dissatisfaction, critical open positions, and suppliers with inconsistent performance. Many of the assumptions supporting the forecast are highly significant but carry considerably less certainty.

Both forecasts produce the same revenue projection, but not the same level of confidence.

Forecasting is more than a planning exercise - it is a process for understanding the future, evaluating confidence, and focusing leadership attention where it can have the greatest impact.

The Ideal Forecast

The ideal forecast is one that allows a business to make their best decisions within an effective window of time, at a cost that is less than the value of improved accuracy, understanding of risk, and speed.

An ideal forecasting process is therefore not simply about producing more accurate numbers. It is about creating timely, actionable insight that helps the organization understand change, evaluate risk, and respond before outcomes are affected.

Rather than relying on periodic meetings to collect assumptions from across the business, the organization maintains an ongoing view of the factors that influence future performance. Forecasting becomes less about assembling information and more about interpreting it.

The process still begins with the forecast itself. Revenue projections, staffing plans, production targets, cash-flow expectations, and strategic initiatives establish a baseline view of the future. However, instead of treating the forecast as a static output that is periodically revisited, the forecast becomes a living model that evolves as business conditions change.

To support this approach, information from across the organization must be continuously connected and evaluated.

Financial systems provide historical performance and current results. CRM platforms provide visibility into pipeline activity, customer health, contract renewals, and sales execution. Operational systems reveal capacity constraints, production performance, maintenance issues, and quality trends. HR systems provide insight into hiring progress, workforce stability, certifications, and staffing gaps. Procurement and supply-chain systems highlight supplier performance, lead times, inventory levels, and sourcing risks.

Equally important is the information that traditionally exists outside structured systems. Contracts, policies, customer communications, supplier correspondence, meeting notes, operational reports, employee interactions, project documentation, and other organizational knowledge often contain early indicators of future risk long before those risks appear in financial results.

Rather than existing in isolation, these signals are evaluated together.

A delayed customer project may increase revenue risk. An open maintenance issue may create production risk. A critical employee resignation may introduce workforce risk. A supplier quality issue may create inventory risk. Individually, these events may appear operational in nature. Collectively, they influence forecast outcomes.

The objective is to move beyond reporting what has happened and begin evaluating what is likely to happen next.

This requires identifying the assumptions that matter most to the forecast and continuously monitoring the indicators that support or challenge those assumptions. As conditions change, the organization's understanding of risk changes as well.

Forecast confidence therefore becomes dynamic rather than static.

A forecast is no longer simply a revenue number, margin projection, or cash-flow estimate. It is accompanied by an understanding of the assumptions driving the forecast, the risks associated with those assumptions, the probability of those risks occurring, and the potential impact if they do.

This allows leadership to distinguish between forecasts that appear identical but carry vastly different levels of certainty.

Just as importantly, the process shifts attention from observation to action.

When risks are identified early, organizations have time to respond. Customer concerns can be addressed before a renewal is lost. Hiring challenges can be mitigated before they impact production. Supplier alternatives can be identified before shortages occur. Maintenance activities can be scheduled before equipment failures affect output.

Forecasting becomes less about explaining variances after they occur and more about influencing outcomes before they occur.

In this environment, forecasting is no longer owned solely by Finance. It becomes a shared organizational capability. Sales, Operations, Procurement, HR, Customer Success, and Finance all contribute information that improves forecast confidence. Technology helps connect those signals, quantify their implications, and surface changes as they occur.

The result is a more informed organization - one that understands not only where it is likely headed, but also what could change that trajectory, how confident it should be in its assumptions, and what actions can be taken to improve the outcome.

A Framework for Forecasting

An effective forecasting process combines traditional forecasting techniques with a structured evaluation of forecast confidence; knowing what we don’t know, and to what degree, is just as important as producing the forecast itself.

The Forecast Confidence Framework

The framework below combines traditional forecasting techniques with a structured process for evaluating and managing forecast confidence.

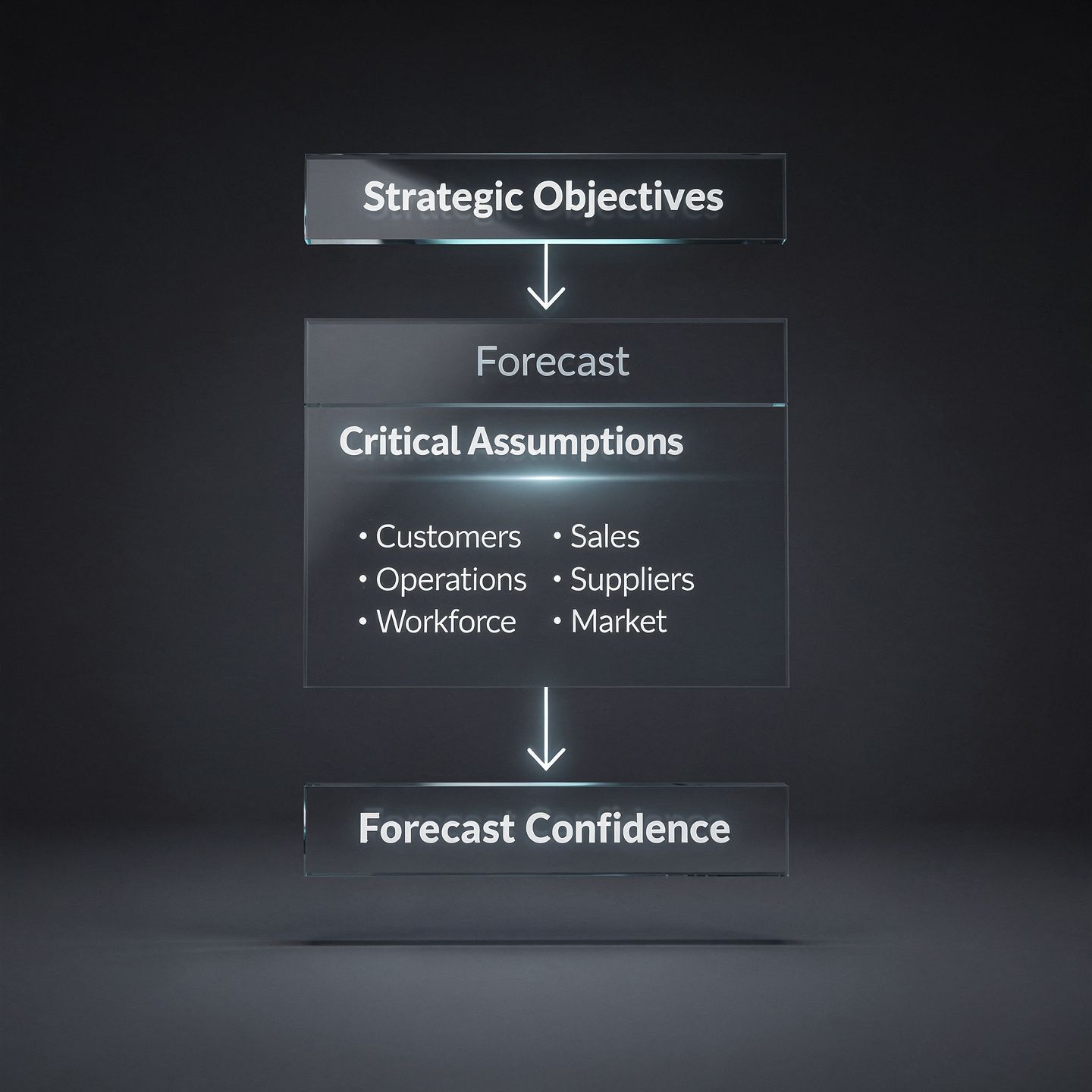

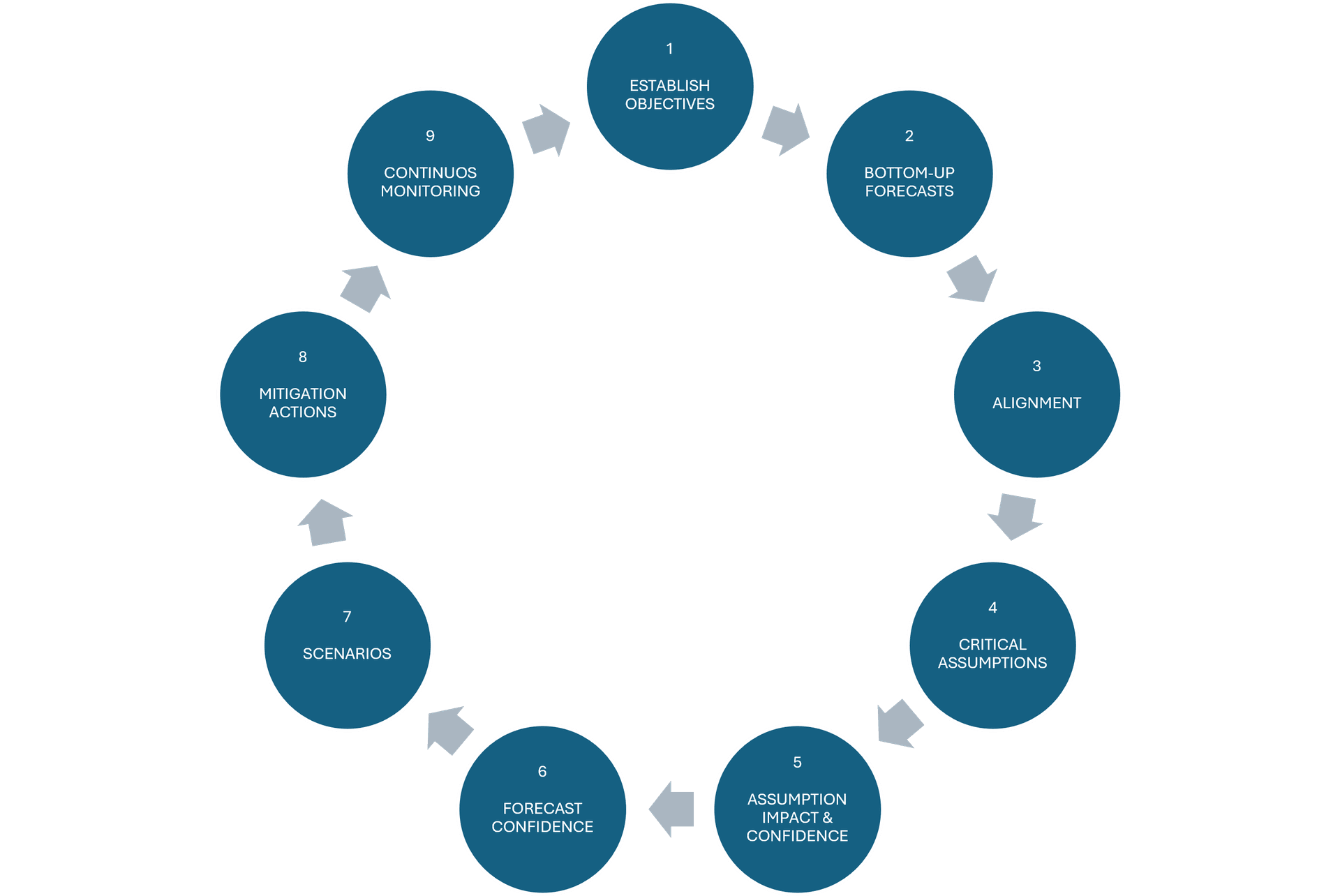

Step 1: Establish Strategic Objectives

The process begins with leadership defining the outcomes the organization is trying to achieve.

Examples include:

- Revenue growth

- Profitability

- Cash flow

- Capacity utilization

- Workforce expansion

- Strategic initiatives

These objectives establish the direction of the planning process.

Output: Strategic objectives

Step 2: Build Bottom-Up Forecasts

Each function develops its forecast based on operational realities.

Sales forecasts demand. Operations forecasts production. HR forecasts workforce requirements. Procurement forecasts supplier capacity. Finance consolidates these inputs into an enterprise forecast.

Output: Functional forecasts

Step 3: Align Top-Down and Bottom-Up Views

Strategic objectives are compared with operational forecasts.

Where differences exist, leaders discuss assumptions, reconcile constraints, and refine plans until an achievable baseline forecast is established.

This alignment process often involves multiple negotiation and review cycles.

Output: Baseline forecast

Step 4: Analyze Critical Assumptions

Every forecast depends on assumptions.

The objective of this step is to identify the assumptions that have the greatest influence on forecast outcomes and evaluate them from two perspectives:

Impact

How much would the forecast change if this assumption proves incorrect?

Impact is typically measured using techniques such as:

- Sensitivity analysis

- Driver analysis

- Historical forecast variance

- Executive judgment

These techniques identify the assumptions that have the greatest influence on revenue, margin, cash flow, capacity, and other key outcomes.

Confidence

How confident are we that this assumption will occur as expected?

Confidence is evaluated using available evidence, including:

- Historical performance

- Leading indicators

- Current business conditions

- Contracts and commitments

- Operational metrics

- Expert judgment

Every critical assumption should ultimately have both an impact assessment and a confidence assessment.

Management attention should naturally focus on assumptions with high impact and lower confidence.

Output: Prioritized assumptions

Step 5: Evaluate Forecast Confidence

Individual assumptions are evaluated together to determine confidence in the overall forecast.

Rather than asking only,

"What is the forecast?"

leadership can also ask,

"How confident are we that we will achieve it?"

The result is a forecast accompanied by a clear understanding of the assumptions that matter most and the confidence associated with each.

Output: Forecast confidence assessment

Step 6: Develop Scenarios

Scenario planning evaluates how forecast outcomes change if critical assumptions change.

Organizations commonly evaluate:

- Expected case

- Upside case

- Downside case

They may also model specific events such as the loss of a major customer, supplier disruptions, delayed hiring, or production constraints.

Scenarios help leadership understand the range of possible outcomes rather than a single point estimate.

Output: Scenario analysis

Step 7: Define Mitigation Actions

Forecast confidence improves when organizations actively manage their most important assumptions.

Mitigation actions may include:

- Customer retention initiatives

- Alternative sourcing strategies

- Capacity investments

- Recruiting acceleration

- Inventory adjustments

The objective is not simply to predict future outcomes but to improve the likelihood of achieving them.

Output: Mitigation plan

Step 8: Monitor and Adapt

Business conditions change continuously.

As new information becomes available, assumptions should be reassessed, confidence updated, scenarios refreshed, and forecasts refined.

Forecasting becomes an ongoing management process rather than a periodic planning exercise.

Output: Living forecast

From Forecasting to Forecast Confidence

Forecasting has never been just about producing numbers. It is about enabling better decisions.

A revenue forecast influences hiring. A production forecast determines capacity investments. A cash flow forecast affects financing decisions. Every forecast becomes an input into dozens of decisions made across the organization.

The quality of those decisions depends not only on the forecast itself, but also on leadership's understanding of the assumptions behind it.

When those assumptions are explicit, their impact is understood, and confidence in them is continuously evaluated, forecasting becomes far more than an annual budgeting exercise or a monthly reporting process. It becomes an ongoing decision-support capability.

Leaders no longer ask only, "What do we expect to happen?"

They also ask:

- Which assumptions matter most?

- How confident are we in those assumptions?

- What evidence supports or challenges them?

- What actions can we take today to improve the likelihood of success?

Those questions fundamentally change how organizations plan, allocate resources, and respond to changing conditions.

Forecast confidence is not a replacement for traditional forecasting. It is the next evolution of it.

Conclusion

Every forecast is ultimately a collection of assumptions about the future.

Some assumptions have little influence on outcomes. Others determine whether strategic objectives are achieved or missed entirely.

The organizations that consistently make better decisions are not those that eliminate uncertainty. Uncertainty is an unavoidable part of business. Rather, they understand which assumptions matter most, continuously evaluate their confidence in those assumptions, and respond as conditions change.

Forecast confidence is the result of that discipline.

Throughout this series, we will explore the most important categories of forecasting assumptions: from revenue and customer retention to workforce, operations, procurement, and cash flow. We will examine practical techniques for measuring their impact, evaluating confidence, and improving forecast quality.

The objective is not simply to build better forecasts - it is to build organizations that make better decisions, faster.